Recent posts

Alarming

How Retail Theft Affects Florida-Based Businesses

01 May 2026

Fur, Fins & Feathers

How To Choose The Ideal Dog Food

28 April 2026

Fur, Fins & Feathers

Mindful Dog Nutrition: Why Quality PET Food Matters

27 April 2026

nichemarket Advice

What Is A Cold Calling Agency?

23 April 2026

Popular posts

Extravaganza

Trending Music Hashtags To Get Your Posts Noticed

24 August 2018

Geek Chic

How To Fix iPhone/iPad Only Charging In Certain Positions

05 July 2020

Extravaganza

Trending Wedding Hashtags To Get Your Posts Noticed

18 September 2018

Money Talks

How To Find Coupons & Vouchers Online In South Africa

28 March 2019

The South African VAT Threshold Chokehold

05 December 2025 | 0 comments | Posted by Che Kohler in nichemarket Advice

For 16 years, South Africa's VAT registration threshold has remained frozen at R1 million—a figure that once represented a generous concession to small businesses but has now become an invisible barrier constraining entrepreneurship, stifling growth, and quietly transferring competitive advantage from emerging enterprises to established corporations.

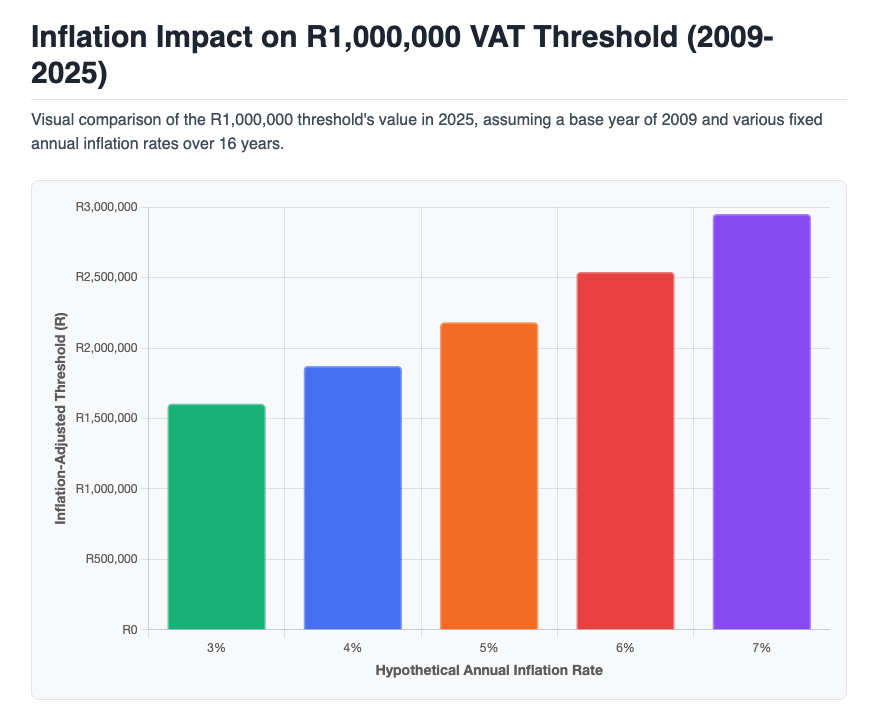

While inflation has steadily eroded the purchasing power of the rand by approximately 100% since 2009, the threshold that determines when businesses must register for VAT has not moved a single cent.

If adjusted for inflation, the R1 million threshold would today sit at approximately R2.1-R2.2 million, effectively meaning that businesses half the size of those originally intended are now being dragged into a complex tax compliance system designed for much larger operations.

This isn't just an administrative inconvenience—it's a structural impediment to small business development that raises fundamental questions about whose interests South Africa's tax policy truly serves.

| Annual Inflation Rate | Inflation Factor (16 Years) | Adjusted 2025 VAT Threshold |

|---|---|---|

| 3% | 1.6047x | R1,604,706 |

| 4% | 1.8730x | R1,872,981 |

| 5% | 2.1829x | R2,182,875 |

| 6% | 2.5404x | R2,540,352 |

| 7% | 2.9522x | R2,952,164 |

| *Base Value: R1,000,000 in 2009 (16 years ago). | ||

The History of VAT in South Africa: From Reform to Rigidity

The Introduction of VAT (1991)

Value-Added Tax was introduced in South Africa on September 30, 1991, replacing the General Sales Tax (GST) that had been in place since July 3, 1978. The switch from GST to VAT represented a fundamental reform of South Africa's consumption tax system, recommended by the Margo Commission in 1986 and outlined in a government White Paper in 1988.

The reform was driven by several compelling factors:

Broader Tax Base: VAT could tax a wider range of services that GST couldn't effectively capture.

Elimination of Tax Cascading: Under GST, taxes were imposed on business inputs, leading to "tax on tax" that particularly burdened capital-intensive industries and made South African exports less competitive internationally.

Reduced Tax Evasion: The GST system relied on exemption certificates that were widely abused due to poor audit trails. VAT's invoice-credit method provided better documentation and traceability.

International Best Practice: By 1991, VAT systems were becoming the global standard for consumption taxation, with over 160 countries eventually adopting the model.

VAT was initially introduced at a rate of 10%, then increased to 14% in April 1993, and most recently raised to 15% in April 2018—the first increase in 25 years. The 2018 increase was part of efforts to address South Africa's fiscal deficit, and a proposed further increase to 15.5% in May 2025 (and 16% in April 2026) was ultimately reversed following political pressure and legal challenges.

The Evolution of VAT Thresholds

When VAT was first introduced in 1991, the registration threshold began modestly. It was subsequently increased from R150,000 to R300,000, recognising the disproportionate burden that VAT compliance placed on very small enterprises.

The significant reform came in 2009, when the threshold was raised to R1 million—more than a threefold increase. This reform was part of a broader initiative to support small businesses and reduce the compliance burden on micro-enterprises. Introduced alongside a simplified turnover tax system for qualifying micro businesses, the R1 million threshold was designed to allow "very small businesses" to focus on growth rather than tax administration.

The thinking was clear and well-intentioned: small businesses with annual turnover below R1 million would be exempt from the complex administrative requirements of VAT, allowing them to invest their limited resources in business development rather than compliance costs.

However, since that 2009 reform, the threshold has not been adjusted once—not for inflation, not for economic conditions, not for the dramatic changes in South Africa's business landscape. For 16 years, that same R1 million figure has remained in place while everything else in the economy has fundamentally changed.

Similarly, related thresholds have been equally neglected:

- The R50,000 voluntary registration threshold has remained unchanged

- The R30 million threshold for monthly (rather than bi-monthly) VAT returns has been frozen since 1991

- The R2.5 million threshold for cash basis accounting (available only to sole proprietors) hasn't moved

This policy paralysis has created what tax experts now describe as "economic distortion" that disproportionately harms the very businesses the threshold was designed to protect.

Why the Current VAT Threshold Keeps Small Businesses from Developing

The Inflation Erosion Effect

The most fundamental problem is straightforward mathematics. R1 million in 2009 is not equivalent to R1 million in 2025. According to multiple tax experts and accounting firms, if the threshold had been adjusted annually for inflation using the Consumer Price Index (CPI), it would now sit between R2.1 million and R2.2 million.

This means that a business earning R83,000 per month (R1 million annually) is now forced into VAT registration—a business that in real economic terms is half the size of those originally intended to be captured by the threshold.

Consider what this means in practical terms:

- A plumbing business with one owner and perhaps an apprentice, earning R83,000 per month in gross turnover

- A freelance consultant invoicing R85,000 per month before expenses

- A small coffee shop with three employees and R90,000 in monthly sales

- A local marketing agency with R100,000 in monthly billings

These are not substantial businesses with sophisticated administrative capacity. These are micro-enterprises where the owner is often still working in the business, wearing multiple hats, and struggling to establish sustainable operations. Yet they're now subject to the same VAT compliance requirements as far larger enterprises.

The Administrative Burden Explosion

When a business crosses the R1 million threshold, the administrative complexity doesn't increase gradually—it explodes immediately. According to industry research and CFO testimonies, crossing the VAT threshold triggers:

Bi-monthly VAT Return Requirements

Unlike larger businesses that file monthly, small businesses must file VAT returns every two months. This means six filing deadlines per year, each requiring:

- Accurate recording of all sales and purchases

- Proper VAT invoice management and storage

- Calculation of output tax (VAT collected) and input tax (VAT paid)

- Electronic submission through SARS eFiling system

- Payment of the difference or claim for refunds

System and Software Requirements

Simple bookkeeping systems are no longer adequate. VAT-registered businesses need:

- VAT-compliant invoicing systems (currently R15,000-R25,000 for setup)

- Accounting software with VAT functionality

- Proper record-keeping infrastructure

- Digital storage and backup systems

Professional Services Costs

Most small business owners don't have the technical expertise to manage VAT compliance themselves, leading to additional costs:

- Monthly accounting fees: R3,000-R8,000

- VAT verification responses: R5,000-R15,000 per verification

- Dispute resolution: R20,000-R50,000+ if SARS disallows input costs

- Annual auditing or review: Additional thousands of rands

Time Burden

Business owners report spending 10-15 hours per month on VAT-related administration—time that could otherwise be invested in business development, client acquisition, product improvement, or strategic planning.

For a business with R1.2 million in turnover, these compliance costs represent 3-5% of revenue—a crushing burden for micro-enterprises often operating on single-digit profit margins.

The Cash Flow Crisis

Perhaps the most devastating impact of VAT registration is the cash flow pressure it creates, particularly for service businesses and those working with slow-paying clients (notably government contracts).

Here's how the cash flow trap works:

The Accrual Accounting Requirement (for companies)

Companies, regardless of size, must account for VAT on an accrual (invoice) basis. This means that VAT becomes payable to SARS when the invoice is issued—not when payment is received.

So a small business that issues an R100,000 invoice (R115,000 including 15% VAT) must pay R15,000 to SARS within the bi-monthly period, even if the client hasn't paid. If the client takes 60, 90, or even 120 days to pay (not uncommon, especially for government contracts), the business must fund the VAT payment from its own limited working capital.

For cash-strapped small businesses, this creates impossible situations:

- They must choose between paying VAT and paying suppliers

- They may need to take on debt to fund VAT payments

- They face penalties and interest if they can't pay on time

- Working capital that should fuel growth is instead tied up in VAT obligations

While sole proprietors and partnerships with turnover below R2.5 million can use cash accounting (paying VAT when they receive payment), this option isn't available to companies—meaning incorporated small businesses face the harshest cash flow impact.

The 15% Price Shock

When a small business crosses the VAT threshold, it faces an impossible choice regarding pricing:

Option 1: Increase Prices by 15%

The business can add VAT to its existing prices, but this makes it 15% more expensive overnight. As tax executive Charles de Wet notes, with the South African Reserve Bank targeting 3% inflation, a 15% price increase is equivalent to five years of inflation-related increases happening in a single moment.

For price-sensitive consumer markets, this can be devastating. Clients who were comfortable paying R1,000 per hour suddenly face R1,150—a psychological barrier that may drive them to competitors who remain below the threshold.

Option 2: Absorb the VAT and Reduce Margins by 15%

Alternatively, the business can keep prices unchanged and simply accept that 15% of the invoice amount must now go to SARS. But this assumes the business has a 15% profit margin to absorb—which many small businesses don't.

According to Deloitte VAT specialist Severus Smuts, most small businesses aren't achieving double-digit profit margins. Absorbing a 15% VAT cost would eliminate profitability entirely for many micro-enterprises.

Option 3: Split the Difference and Lose on Both Ends

Some businesses try to compromise—raising prices by 7-8% and absorbing the rest. This means they become less competitive while also reducing their margins, creating a double squeeze that makes sustainable operation nearly impossible.

The Competitive Distortion and the "Cliff Effect"

The static VAT threshold creates severe market distortions around the R1 million mark. Tax experts describe this as a "cliff effect" where businesses face powerful disincentives to grow.

Bunching Below the Threshold

Anecdotal evidence and tax practitioner observations reveal that many businesses deliberately limit their growth to stay below R1 million. A Cape Town marketing agency reported to ThriveCFO that they began "artificially limiting client acquisition" when approaching R900,000 in turnover to avoid VAT registration.

This behaviour is economically rational from the business owner's perspective but disastrous for economic development. Businesses that should be hiring employees, taking on larger contracts, and expanding their operations instead deliberately constrain themselves to avoid crossing an arbitrary threshold.

Uneven Playing Fields

The threshold creates fundamentally unfair competition. Consider two similar businesses:

- Business A: R990,000 annual turnover, not VAT registered, charges R1,000 per service

- Business B: R1,100,000 annual turnover, VAT registered, must charge R1,150 for the same service (or absorb costs and reduce margins)

Business B is being penalised for growing by R110,000 more than Business A, even though both are clearly micro-enterprises. This creates perverse incentives and undermines the principle that competitive markets should reward growth and efficiency.

The Service Industry Trap

The distortion is particularly severe for service businesses selling to consumers (B2C) rather than other businesses (B2B).

When a VAT-registered business sells to another VAT-registered business, the client can claim the VAT as an input tax credit, making the VAT effectively neutral from their perspective. But when selling to consumers who can't claim input tax, the full 15% becomes a real price increase that the business must either pass on (losing price competitiveness) or absorb (destroying margins).

South African VAT legislation makes no distinction between B2B and B2C businesses when determining threshold requirements, meaning that plumbers, electricians, consultants, and other service providers selling primarily to consumers face the harshest competitive impact.

The Compliance Cost Trap: A Hidden Tax on Growth

Beyond the direct costs of VAT compliance, there are indirect costs that represent an even greater barrier to small business development:

The Opportunity Cost

When a small business owner spends 10-15 hours per month managing VAT compliance, that's 10-15 hours not spent on:

- Developing new products or services

- Building client relationships

- Marketing and business development

- Strategic planning

- Employee training and development

- Innovation and improvement

For businesses in their critical early growth phases, these opportunity costs can determine whether the business scales successfully or remains permanently stunted at just above the threshold level.

The Risk and Penalty Exposure

VAT is complex and nuanced. Even with professional help, mistakes happen. When they do, the consequences can be severe:

Input Tax Disallowances

SARS may disallow input tax claims for various technical reasons—incorrect invoice format, missing documentation, timing errors, or classification issues. When this happens, the business must pay back the claimed input tax plus interest and potentially penalties.

For a small business that claimed R50,000 in input tax that gets disallowed, the financial impact can be catastrophic.

Verification Requests

SARS regularly conducts VAT verifications, requiring businesses to provide detailed documentation and explanations. Responding to a verification request typically costs R5,000-R15,000 in professional fees, plus the time burden of gathering documentation.

Dispute Resolution

If a verification escalates into a dispute, the costs explode. Legal and accounting fees for tax disputes commonly reach R20,000-R50,000 or more—amounts that can bankrupt a small business even if they ultimately prevail.

The Knowledge and Skills Gap

Small business owners are typically experts in their trade—plumbing, marketing, consulting, manufacturing—not in tax law. VAT is sufficiently complex that even tax professionals specialise in it.

Expecting a plumber earning R90,000 per month to understand the nuances of time of supply rules, apportionment calculations, zero-rated versus exempt supplies, and the proper format for tax invoices is unrealistic. Yet failure to comply correctly carries serious consequences.

This creates a dependency on professional services that small businesses can often ill afford, further draining resources that should be invested in growth.

How the Current Threshold Benefits Big Business While Blocking Competition

The frozen VAT threshold isn't just a burden on small businesses—it's a competitive barrier that protects established large corporations from disruptive competition. This effect, while perhaps unintended, operates through several mechanisms:

Artificial Barriers to Entry and Scale

New entrants to markets must either:

- Remain deliberately small to stay below the threshold, limiting their ability to compete with established players

- Accept the compliance burden early in their development, diverting critical resources away from competition

Established businesses, by contrast, have already absorbed VAT compliance costs, have dedicated accounting staff, have sophisticated systems in place, and have the working capital to manage VAT cash flow requirements.

This creates a moat around incumbent businesses. A startup trying to disrupt an established market faces not just the normal challenges of competition, but an additional administrative and financial burden that kicks in precisely when they're beginning to gain traction.

Suppressed Competitive Pressure

When potential competitors deliberately limit growth to avoid VAT registration, the competitive pressure on established businesses diminishes. Markets become less dynamic, with fewer challengers emerging to drive innovation and efficiency.

Consider a sector dominated by several large VAT-registered companies. Small competitors who might otherwise grow to challenge these incumbents instead hit the R1 million threshold and face the choice of either:

- Stopping growth and remaining no threat

- Crossing the threshold and facing immediate cost disadvantages

Either outcome protects the market position of established players.

The Investment and Expansion Advantage

Large corporations can spread the fixed costs of VAT compliance across much larger revenue bases. A business with R50 million in turnover can afford dedicated tax staff, sophisticated systems, and professional advisory services. The proportional burden is minimal.

A business with R1.2 million in turnover bears the same absolute compliance costs, but they represent a crushing 3-5% of revenue. This fundamentally different cost structure makes it harder for small businesses to price competitively, invest in growth, or weather economic shocks.

Regulatory Capture Through Complexity

The more complex the regulatory environment, the more it favours large, sophisticated players over small, nimble competitors. Complex VAT rules require expertise that only large businesses can afford to maintain in-house. They can hire specialists, invest in training, maintain relationships with SARS, and navigate disputes effectively.

Small businesses must either pay for this expertise (at rates they can barely afford) or attempt to manage compliance themselves (risking costly errors).

This creates a form of regulatory advantage where market success depends not just on product quality, customer service, or operational efficiency, but on the ability to navigate complex tax compliance requirements.

The Government's Revenue Incentive

Why has the threshold remained frozen for 16 years despite obvious economic distortions and widespread calls for reform from tax experts, business organisations, and small business advocates?

The uncomfortable answer appears to be revenue protection.

Revenue Concerns

According to tax specialists, National Treasury and SARS are reluctant to raise the threshold because:

- A lower threshold brings more businesses into the VAT net

- More registered vendors means more revenue collection

- Many small businesses sell directly to consumers who can't claim VAT, making them pure revenue sources

- Raising the threshold could reduce revenue collections, creating budgetary pressure

This creates a fundamental conflict: What's good for small business development (a higher threshold) appears bad for government revenue (fewer registered vendors). In an environment of chronic budget deficits and revenue pressures, the revenue consideration consistently wins.

Political Sensitivity

As multiple tax experts note, any Finance Minister who touches VAT becomes unpopular. When Enoch Godongwana attempted to raise the VAT rate from 15% to 15.5% in early 2025, the political backlash was so severe that the government ultimately reversed the decision before it could take effect.

If raising the VAT rate is politically explosive, increasing the threshold (which reduces revenue) is even more challenging. Politicians are reluctant to be seen as providing "tax relief for business owners" when social spending demands are urgent.

Administrative Justifications

SARS may also see administrative benefits in more registered vendors:

- More formal vendors discourage informal trading

- Broader VAT coverage improves compliance culture

- A larger registered base provides better data for enforcement

While these administrative considerations have merit, they prioritise the tax authority's convenience over the economic development impact on small businesses.

International Comparisons: South Africa Is Falling Behind

Looking at how other countries handle VAT thresholds provides an important perspective on whether South Africa's approach is reasonable or an outlier.

Developed Economies

United Kingdom: £85,000 (approximately R2.1 million)

- The UK has one of the highest VAT thresholds globally

- It's regularly reviewed and adjusted

- Reflects recognition that micro-businesses need protection from compliance burdens

Australia: A$75,000 (approximately R1 million)

- Similar to South Africa's nominal threshold

- But Australia has simplified compliance requirements

- Regular reviews ensure alignment with economic conditions

European Union: €12,500 to €50,000 depending on country

- Wide variation reflects different economic scales

- Most countries regularly adjust thresholds

- Many offer simplified schemes for small businesses

France, Japan: Thresholds around R2 million equivalent

- Higher thresholds recognise the disproportionate burden on micro-enterprises

- Reflect policy priority on supporting small business development

Comparable African Economies

Kenya: Regularly reviews and adjusts both turnover tax and VAT thresholds

- Demonstrates that even developing economies prioritise threshold maintenance

- Recognises the growth implications of static thresholds

Namibia: Similar threshold levels to South Africa

- But with simpler compliance requirements

- More flexibility in administration

Ghana: Recently raised VAT threshold to approximately US$40,000 (R750,000)

- Part of broader tax reform to ease pressure on SMEs

- Recognised that narrow VAT bases on micro-enterprises were administratively inefficient

- Prioritised sustainable economic growth over marginal revenue collection

The South African Anomaly

What makes South Africa's situation unique is not the nominal threshold level—R1 million is roughly comparable to many developed economies. The problem is the 16-year freeze without adjustment.

Most countries with similar thresholds:

- Review them regularly (every 1-5 years)

- Adjust for inflation automatically or periodically

- Simplify compliance for small businesses near the threshold

- Offer transition support or phased implementation

South Africa does none of these. The threshold has simply been abandoned at a 2009 level, while the economy has fundamentally transformed around it.

The Path Forward: Policy Solutions for Fair VAT Thresholds

Multiple tax experts, business organisations, and accounting professionals have proposed reforms that would address the threshold problem without sacrificing tax revenue or administrative efficiency:

Immediate Inflation Adjustment

Proposal: Raise the threshold to R2.1-R2.2 million to restore its 2009 real value

This would:

- Eliminate the most obvious injustice of forcing businesses half the intended size into VAT registration

- Provide immediate relief to micro-enterprises at the critical growth stage

- Restore the original policy intent from 2009

- Free up resources for business development rather than compliance costs

Implementation: Could be done through an amendment in a single budget cycle

Automatic Annual Indexation

Proposal: Link the threshold to inflation so it adjusts each year automatically

This would:

- Prevent the problem from recurring

- Remove the political difficulty of periodic threshold increases

- Ensure the threshold maintains its real value over time

- Provide businesses with predictable rules for planning

Implementation: Requires legislative amendment to VAT Act to include an indexation formula

Simplified Compliance for Small Vendors

Proposal: Create a simplified VAT regime for businesses between R1 million and R3 million

This could include:

- Quarterly rather than bi-monthly returns

- Simplified record-keeping requirements

- Flat-rate schemes based on industry sector

- Reduced verification frequency

- Cash accounting availability for all business types (not just sole proprietors)

Implementation: Would require regulatory changes but not full legislative amendment

Phased Entry System

Proposal: Create a grace period or phased compliance system when businesses first cross the threshold

For example:

- First year: Registration required but simplified compliance

- Second year: Full compliance requirements phase in

- Transition support and education provided

This would:

- Reduce the "cliff effect" shock

- Allow businesses to adapt gradually

- Encourage voluntary compliance through a supportive rather than a punitive approach

Business-Type Differentiation

Proposal: Consider different thresholds for B2C versus B2B businesses

The competitive distortion is much more severe for businesses selling to consumers. A differential threshold (e.g., R2 million for B2C, R1 million for B2B) would:

- Address the most severe competitive inequities

- Recognise that VAT collected from B2B transactions is mostly neutral

- Focus compliance resources on businesses where VAT creates real revenue

Political Will and Policy Priorities

Ultimately, threshold reform requires political courage. It means:

- Accepting short-term revenue reduction for long-term economic growth

- Prioritising small business development over administrative convenience

- Recognising that over-taxing micro-enterprises is economically counterproductive

- Understanding that a thriving small business sector generates more tax revenue in the medium to long term than squeezing micro-enterprises in the short term

The Broader Economic Implications

The frozen VAT threshold isn't just a tax policy issue—it's an economic development crisis with implications for:

Job Creation

Small businesses are South Africa's primary source of new job creation. When these businesses are forced to divert resources to tax compliance rather than growth, employment suffers. When businesses deliberately limit growth to avoid VAT registration, they don't hire the additional employees they otherwise would.

Entrepreneurship and Innovation

Young, innovative businesses are disproportionately harmed by premature VAT registration. A tech startup, marketing agency, or specialised service provider might reach R1 million in turnover while still operating at a loss (high revenue, but higher expenses). Forcing VAT compliance at this stage can be the difference between survival and closure.

Formalisation of the Economy

Ironically, an overly burdensome VAT threshold may actually reduce formalisation. Some businesses may choose to remain informal or under-report income specifically to avoid crossing the threshold. A more reasonable threshold, combined with simplified compliance, would encourage voluntary formalisation.

Economic Growth

When thousands of businesses deliberately limit their growth, the cumulative impact on GDP is substantial. The OECD and World Bank research consistently shows that reducing compliance burdens on small businesses generates significant economic returns through accelerated growth and job creation.

Inequality and Concentration

By protecting established businesses from competitive disruption, the frozen threshold contributes to economic concentration. When markets are less competitive, dominant players can maintain higher margins and slower innovation. This concentrates wealth in established corporations rather than distributing it through a vibrant small business sector.

Time for Reform

South Africa's R1 million VAT threshold represents a policy failure with profound consequences for economic development, entrepreneurship, and competitive markets. What began in 2009 as a progressive reform to support small businesses has, through 16 years of neglect, become a barrier to the very growth it was meant to encourage.

The frozen threshold is not just inefficient—it's actively harmful. It forces micro-enterprises into complex compliance systems they're not equipped to manage. It creates cash flow crises for businesses operating on thin margins. It discourages growth at precisely the moment when businesses should be scaling. And it protects established players from competitive disruption.

The math is simple, and the injustice is clear: R1 million in 2009 is not R1 million in 2025. Businesses half the size originally intended are now bearing burdens designed for much larger operations.

Tax experts, business organisations, accounting professionals, and small business advocates have spoken with remarkable consensus: the threshold must be raised, indexed to inflation, and paired with simplified compliance for smaller vendors.

The barriers to reform are not technical but political: revenue concerns and the political sensitivity of tax changes. But this short-term thinking sacrifices long-term economic growth for immediate fiscal convenience.

A thriving small business sector generates employment, drives innovation, creates competition, distributes wealth, and ultimately produces far more tax revenue than can be squeezed from struggling micro-enterprises forced into premature VAT compliance.

South Africa's small businesses deserve a tax system that supports their success, not one frozen in 2009 while the economy has moved on. The frozen VAT threshold isn't just an outdated policy—it's a structural impediment to the economic dynamism South Africa desperately needs.

It's time for reform. It's time to raise the threshold. And it's time to stop protecting big business at the expense of small business development.

The views expressed in this article represent an analysis of publicly available tax policy research, expert testimony, and industry data. Business owners should consult with qualified tax professionals regarding their specific VAT obligations and compliance requirements.

You might also like

How Retail Theft Affects Florida-Based Businesses

01 May 2026

Posted by Che Kohler in Alarming

A look into how much retail theft costs stores across Florida, what the down stream impacts are and what you can do to reduce your risk as a shop own...

Read more

What Is Search Everywhere?

06 April 2026

Posted by Che Kohler in nichemarket Advice

How SEO managers will have to adapt to users finding content via social media, LLMs and forums and why strategies will need to adapt to tap into thos...

Read more{{comment.sUserName}}

{{comment.iDayLastEdit}} day ago

{{comment.iDayLastEdit}} days ago